Don’t stand so close to me by Wendy Grossman

Originally posted on pelicancrossing.net on March 11th 2016

At last week’s Internet Law Works-in-Progress – a New York Law School invitation event where lawyers play hooky by critiquing each other’s half-finished papers – Nizan Geslevich-Packin and Yafit Lev-Aretz came up with an intriguing idea: the right to be unnetworked. “Tell me who your friends are and I will tell you who you are,” their paper’s abstract begins.

Their idea is inspired by concerns about alternative forms of credit scoring for people whose histories aren’t a good match for the commercial methods currently in use, This looks like a good thing for making traditional credit-scoring less rigid. People who’ve never had loans are considered terrible risks (no payment history), and 12 to 15% of the US population are unbanked or underbanked, and their lack of access to financial services is a vicious circle of self-fulfilling prophecies.

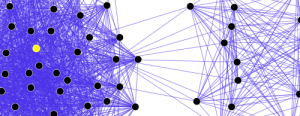

So: use all that webby stuff you can find out about them instead, like websites, Wikipedia pages, and social media presence. My social graph, of such interest to security agencies and law enforcement in determining whether I’m dangerous, can serve a similar function for banks.

So: use all that webby stuff you can find out about them instead, like websites, Wikipedia pages, and social media presence. My social graph, of such interest to security agencies and law enforcement in determining whether I’m dangerous, can serve a similar function for banks.

When applied to financial services, this idea is not unlike the future outlined by Consult Hyperion‘s technical director, Dave Birch in his 2014 book Identity is the New Money. In it, Birch proposes that we have come full circle: centuries ago, your word was your bond, and today, given digital payments and all-knowing smartphones, it can be again. As I might have back then, I currently owe my local shop 33p, and I have this credit (as small as it is) because they know from 25 years’ experience that I will settle that next time I’m in with enough change. Their experience and recognition of my person is my bond. That’s great if you’re long-established in a friendly neighborhood where the shops are run by their owners personally.

This is not most people’s lives, and so we keep devising substitutes for that personal knowledge. Strangers don’t have to trust you if they can trust the form of money you give them, whether that’s physical cash (guaranteed by a government), a credit card (a bank), or a bitcoin (technology). And so to social credit. Would you give a loan officer your Facebook password? How much do you want the loan?

In this game, as Geslevich-Packin and Lev-Aretz analyze it, the richest people – not measured numerically but by the amount of need for debt to finance one’s lifestyle – have the best option. They can simply refuse to participate. It’s a version of “fuck-you money” in Hollywood. There it means enough money that you don’t have to take crap from anyone you don’t want to. Here, enough money means never having to tell your bank you’re my friend.

In this game, as Geslevich-Packin and Lev-Aretz analyze it, the richest people – not measured numerically but by the amount of need for debt to finance one’s lifestyle – have the best option. They can simply refuse to participate. It’s a version of “fuck-you money” in Hollywood. There it means enough money that you don’t have to take crap from anyone you don’t want to. Here, enough money means never having to tell your bank you’re my friend.

And you might be wise not to. I slum around with a lot of low-lifes – folksingers (perennially broke), serial entrepreneurs (high-risk), and people I know nothing about who requested I add them to my Friends list and who for all I know are dangerous weirdos. With a little care and forethought, however, a reputation rescuer might be able to prune my profile to highlight an Ivy League education and the more respectable of my journalism credits. The presence of Labour Deputy Leader Tom Watson in my Twitter and Facebook profile pictures (several people away and ignoring me) could cut either way.

Geslevitch-Pakin and Lev-Aretz talk about these strategies. Your rich-enough-to-say-hell-no person can afford to be Type A, refusing to play and choosing privacy over financial assistance. Type B optimizes as above, deleting the damaging connections to all those folksingers and goofballs, and sucking up to the ones wearing suits in their photos, just as ambitious students maximize their chances of getting into the fancy university or high-paying job of their choice by carefully curating their activities and social presence. Type C would like to be smart like A or B and has the assets to do so, but is too lazy, passive, or ignorant to manage it. Type D would also like to be smart, but knowing they are poor candidates, seek to hide their flaws by avoiding social networks altogether – more likely to brand them deadbeats (the authors’ term: “lemons”) than credit-worthy. Either way, the overall result is to invade the privacy of the third parties in everyone’s social circle, who are not consulted in these arrangements; decrease social mobility; and institutionalize discrimination.

Therefore: the right to be unnetworked, the authors’ suggestion for limiting and regulating social scoring. Many details remain for discussion, but there are two reasons I like the concept. The first is that the aggregated data on today’s social networks was not supplied with credit scoring in mind; it’s more authentic than similar posted information 20 years’ hence will be if social scoring continues. Using this information for credit assessment is a distinct change of use. The other reason is that it seems to me to derive logically from the American Fifth Amendment, the one that allows you to refuse to testify on the basis that you may incriminate yourself; the UK equivalent used to be the right to silence. Seems to me, that right ought to extend to refusing to supply my Facebook password to an inquisitive loan shark.

Wendy M. Grossman is the 2013 winner of the Enigma Award. Her Web site has an extensive archive of her books, articles, and music, and an archive of earlier columns in this series. Stories about the border wars between cyberspace and real life are posted occasionally during the week at the net.wars Pinboard – or follow on Twitter.